In 2014, Nigeria, under Goodluck Jonathan, proudly reclaimed its position as Africa’s largest economy after a historic Gross Domestic Product (GDP) rebasing.

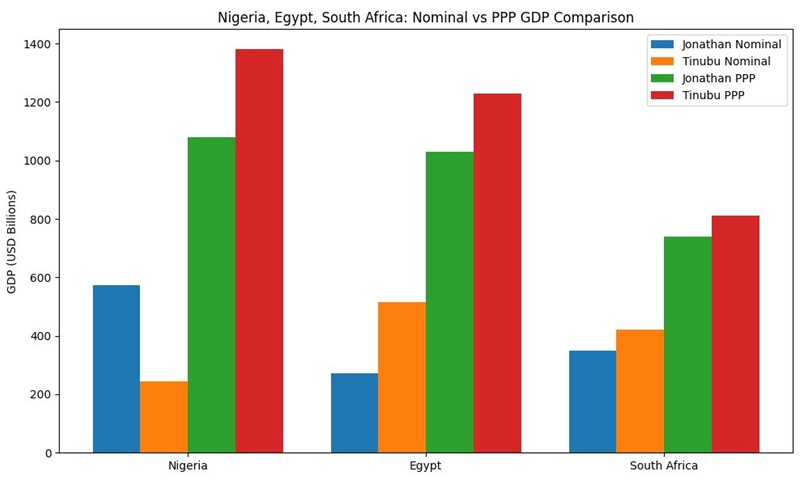

Nominal figures in US dollars hovered near $574 billion, while real economic output — measured in purchasing-power parity (PPP) — confirmed that Nigeria’s domestic economy was robust and growing.

Yet, even as critics hurled political insults — labeling Jonathan a “Kindergarten President” or “Clueless” — the fundamentals of the Nigerian economy were improving. Achievement, it seemed, was quietly happening without the theatrics of overpromising or hyperbole.

Fast forward a decade, and the picture is starkly different. Under Bola Ahmed Tinubu, Nigeria’s nominal GDP has fallen to approximately $244 billion, a drop of over 50% in dollar terms.

Compare this with Egypt, whose economy surged past Nigeria’s nominal GDP to around $516 billion, or South Africa, steadily growing to $420 billion.

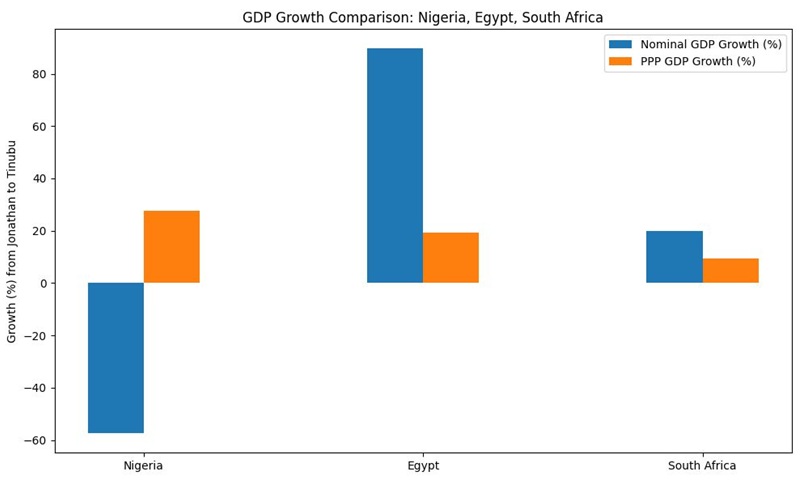

On the surface, the numbers suggest stagnation or even regression. And indeed, in dollar terms, they do.

But the story gets more telling when we look at PPP-adjusted GDP, which strips away the distortions of currency devaluation.

Nigeria’s real domestic economy continues to grow, registering about $1.38 trillion in PPP terms, an increase of roughly 28% since Jonathan’s era.

Egypt and South Africa, while growing, lag behind in real output.

This disparity between nominal and real measures is not just technical; it is a mirror reflecting the failure of political leadership to translate domestic productivity into global credibility.

The lesson is clear: rhetoric and theatrics cannot substitute for sound economic management.

Political leaders who boast and belittle predecessors while ignoring structural vulnerabilities — from currency instability to overreliance on oil — are failing the nation.

Nigeria’s real economy may still be strong, but its international image, investor confidence, and living standards are eroded by mismanagement, indecision, and a preference for spectacle over strategy.

It is time Nigerians demand leaders who focus on sustainable growth, diversification, and fiscal prudence, rather than hollow slogans and partisan theatrics.

Achievement is not measured by insults or campaigns; it is measured by the health of the economy, the resilience of citizens, and the ability to secure a future that is economically sovereign and socially just.

If Nigeria’s politicians cannot see this, the numbers will continue to speak for themselves — quietly, painfully, and unarguably.